By Shabir Ladha, CPA, CA, FEA, ICD.D

Shabir Ladha is a Chartered Professional Accountant with extensive experience in financial reporting, valuation, and transaction advisory. He works closely with business owners, leadership teams, and advisory groups on matters related to ownership transition, financial readiness, and long-term value creation. Shabir brings a disciplined, practical approach to complex financial issues. His work supports organizations through growth, restructuring, and succession by helping leaders understand what the numbers are truly telling them. He believes that clarity, preparation, and coordination are essential to any successful transition.

Succession planning is a journey, not an event. Unless it is unplanned.

In many cases, the conversation only begins after a health scare, unexpected disruption, or forced transition. When that happens, families and leadership teams are left making complex financial decisions under pressure. Grief, uncertainty, and operational strain collide with questions about liquidity, valuation, tax, and sustainability.

From an accounting perspective, succession often begins with one simple question:

Can the business support the transition being contemplated?

Financial clarity does not eliminate complexity. But it prevents unnecessary surprises.

Accounting plays a quiet but critical role in succession. When done well, it brings discipline, realism, and confidence to decisions that affect ownership, family, and business continuity. When overlooked, it introduces risk at precisely the moment stability is most needed.

What’s Commonly Misunderstood

One of the most common misconceptions is that accounting’s role in succession is limited to tax planning. While tax efficiency is important, it is only one part of a much broader financial picture.

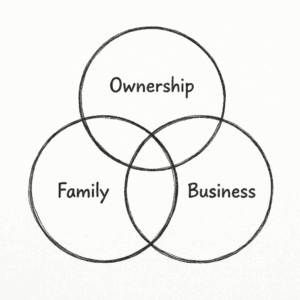

Historically, succession planning has often centered on ownership transition and the associated tax strategy. That may involve estate freezes, reorganizations, trusts, or capital gains planning. But ownership is only one circle in a broader system.

Financial statements are frequently prepared for compliance or lender reporting, not for transition readiness. Owner compensation, discretionary expenses, and one-time decisions can obscure the true economic performance of the business. A company may appear strong on paper while masking structural issues that become visible during transition.

Another misunderstanding is treating valuation as a single event rather than the outcome of consistent financial discipline over time. Value is built, protected, or eroded long before succession discussions begin.

Succession planning requires accounting to look forward, not just backward.

Where the Risk Becomes Real

Accounting-related risk surfaces when assumptions are tested under pressure.

When a triggering event occurs, whether illness, incapacity, conflict, or forced exit, questions arise quickly. Is there sufficient liquidity? Can the business support debt required for a buyout? Will working capital remain adequate during leadership change? Are valuation expectations realistic?

Risk becomes real when:

- Earnings have not been normalized to reflect true operating performance

- Owner-specific expenses distort financial results

- Working capital requirements are misunderstood

- Debt capacity has not been stress-tested

- Financial reporting lacks credibility or consistency

- Valuation expectations exceed financial reality

In these moments, flexibility narrows. Decisions that could have been phased become rushed. Accounting gaps limit options.

The Role of Accounting in Succession

Accounting does not determine who should lead or who should own. Its role is to ensure the financial foundation can support those decisions across ownership, family, and business.

When succession planning is approached intentionally, accounting helps to:

- Clarify sustainable earnings and cash flow

- Establish realistic valuation grounded in financial performance

- Assess whether the business can fund transition without destabilizing operations

- Identify value drivers that can be strengthened before transition

- Provide confidence to successors, lenders, and stakeholders

Accounting provides structure. It translates aspiration into financial reality. Without that foundation, even well-designed legal or insurance strategies can struggle.

Why Coordination Matters

Accounting sits at the center of succession decisions.

- Ownership structures depend on financial assumptions.

- Tax strategies rely on accurate valuation.

- Insurance funding must reflect realistic financial capacity.

- Leadership transition timelines must align with cash flow and stability.

When advisors work from different numbers or conflicting assumptions, even well-intentioned plans can create friction. Succession planning works best when accounting is integrated into a coordinated advisory process. Alignment across legal, tax, insurance, and leadership planning ensures that decisions are grounded in the same financial reality.

Shabir’s Resources

Succession planning is a journey not an event unless it is unplanned. A health scare can often be the trigger and sadly in some cases the health event isn’t the catalyst that starts the planning, but it forces an instant succession. In those cases, succession becomes a chaotic time where close friends and family are forced to push aside the grieving process to ensure the business can endure, employees are taken care of, customers are satisfied and the income that the family has relied up on from the business continues to be there as needed.

When the conversation does start, it can often start with the accountant and tax advisor. That can lead to planning around ownership transition. Historically, that is what succession planning has been; the transition around ownership of the company which deals with a tax plan to defer as much as possible, the setup of a family trust or other creative plans. The problem is that ownership is but one piece of the three-circle model.

What will management of the business look like? Regardless of which leadership roles have been filed by owners, a plan for leadership succession (Business Circle) is often more important for business success than ownership success. Ignoring the impact on the family is also a mistake. The family will normally be reliant on the business to fund their lifestyle, the business if often the family’s identity and it serves to fill their days. Ultimately, when all three circles are planned for, the family, the business and the owners are setup for a successful transition allowing for a long-term legacy.

While working with the right advisors is a good idea, the most important step to take is the first one. The list below can be a starting point for conversations to begin the process:

Ownership

Ownership transition is often the first place succession conversations begin, particularly when accountants and tax advisors are involved. While ownership structure and tax efficiency are critical, they represent only one part of the succession picture.

From an accounting perspective, ownership planning requires clarity around:

- Succession Objectives

Define what “success” looks like: maximum sale price, family continuity, employee ownership.

- Ownership Structure Review

Analyze current share structure, shareholder agreements, and whether an estate freeze, reorganization, or trust structure is appropriate.

- Tax Planning Strategy

Evaluate lifetime capital gains exemption eligibility, estate freezes, family trusts, pipeline planning, and tax implications of selling vs. transitioning to family or management.

- Valuation & Value Drivers

Obtain a realistic business valuation and identify the operational, financial, and strategic levers that could increase value before transition.

- Legal Risk Review

Update shareholder agreements, buy-sell clauses and contingency plans for unexpected events.

- Timeline & Transition Phasing

Build a realistic multi-year roadmap which will align with the ownership transition plan.

Family

Ignoring the financial impact of succession on the family is one of the most common and costly mistakes. Families are often financially reliant on the business, emotionally connected to it, and deeply affected by how transition unfolds. Accounting plays a key role in translating family goals into financial reality.

Key considerations include:

- Personal Readiness & Future Vision

Clarify your post-transition goals: lifestyle, income needs, continued involvement (if any), and personal identity beyond the business

- Succession Objectives

Define what “success” looks like: family continuity, legacy preservation, family harmony.

- Governance Structure

Introduce or strengthen family meetings and family councils to assist with decision making.

- Estate & Will Alignment

Ensure wills, powers of attorney, and estate plans are aligned with the business transition plan to avoid conflicts or unintended tax consequences.

- Timeline & Transition Phasing

Build a realistic multi-year roadmap that satisfied personal and family needs

Business

Ultimately, the success of any succession plan depends on the financial health of the business itself. Regardless of ownership outcomes, the business must be able to operate, grow, and withstand disruption.

From an accounting perspective, this includes:

- Succession Objectives

Define what “success” looks like: management transition, culture & strategy

- Successor Identification & Development

Assess whether successors exist internally (family or management) and create a structured development plan to build leadership, decision-making, and credibility.

- Leadership Continuity Beyond the CEO

Map key roles across the organization and ensure there is bench strength.

- Governance Structure

Introduce or strengthen leadership teams or advisory councils.

- Financial Readiness of the Business

Assess normalized earnings, working capital needs, debt capacity, and whether the company can support the transition plan.

- Cultural Continuity

Ensure successors understand they are inheriting stewardship, not just authority.

- Strategic Direction Post-Transition

Confirm that there is a clear strategic plan that extends beyond the founder, giving confidence to employees, lenders, and stakeholders.

- Communication Plan

Determine what to communicate, to whom, and when including family, leadership team, employees, customers, suppliers, and lenders.

- Timeline & Transition Phasing

Build a realistic multi-year roadmap that phases leadership transfer.